Understanding Wholesale Voice: Key Insights and Benefits

What wholesale voice is, how termination works, top providers, cost benefits, future trends (5G, AI, blockchain), and how to choose the right solution.

Tier-1 termination, least-cost routing, voice quality scoring, peering exchanges, and the fraud patterns every carrier sees — written for the network architects and procurement leads who buy voice at scale.

Wholesale voice is the part of the telecom industry that consumers never see and procurement teams rarely talk about in public. It is a market of carriers selling voice minutes to carriers, of weekly rate cards renegotiated by the row, of routing engines that re-optimise every call against quality and cost in real time. Every business call that crosses a country border touches at least one wholesale voice contract on its way to the destination handset.

This guide is for the operators and procurement leads who buy that capacity. It covers what the market actually is, how Tier-1, Tier-2, and grey routes differ, the routing engine that decides which path each call takes, the quality metrics that signal a route going bad, the settlement and CDR-audit clauses that protect you from a bad invoice, and the fraud patterns that cost the unprepared real money. Read straight through or skim the section you need.

Wholesale voice is the business of carriers and large platforms buying voice minutes from each other in bulk, then either consuming them internally or reselling them downstream. It is the part of the telecom industry that consumers never see, but every cross-border business call moves through it.

The market is huge. Hundreds of carriers, dozens of voice exchanges, thousands of rate cards updated weekly. A single international call from a US contact centre to a customer in Brazil might traverse three different carriers — and each leg is paid for under a separate wholesale agreement priced in fractions of a cent per minute.

Buyers are operators of voice platforms: contact centres, BPOs, SIP trunk resellers, CPaaS providers, wholesale carriers themselves, and enterprises with serious international traffic. Sellers are Tier-1 carriers, regional operators, and aggregators that consolidate routes from many upstream providers.

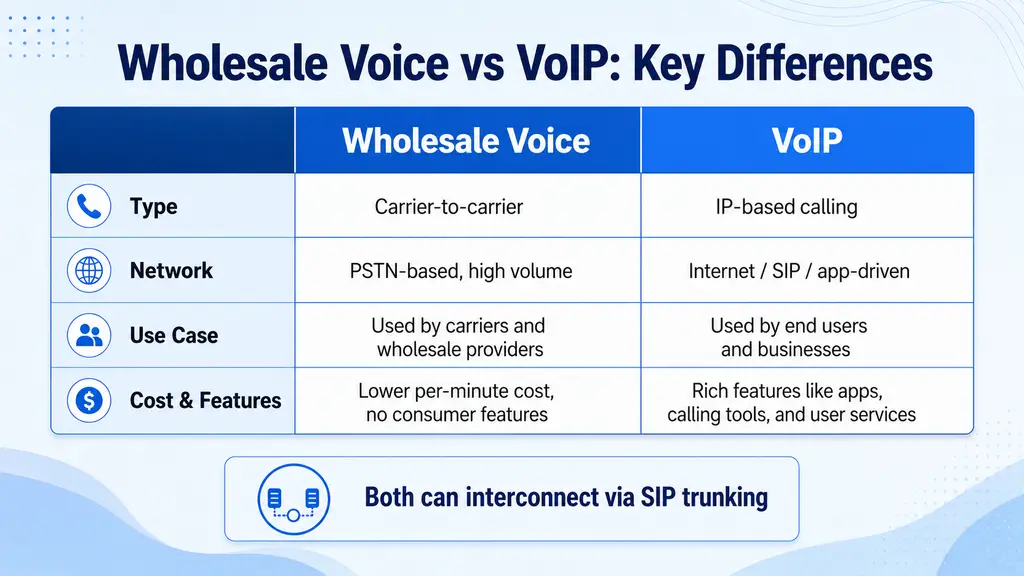

The two terms overlap heavily, but they are not identical. Wholesale voice is the broader business — the buying and selling of voice minutes between carriers, regardless of the underlying technology. Wholesale VoIP is the subset where the transport is IP, almost always over SIP.

In 2026, more than 95% of wholesale voice in mature markets is also wholesale VoIP. Legacy TDM (time-division multiplexing) interconnects still exist in some emerging-market termination scenarios, but the trend has been one-way for two decades. When a procurement team writes "wholesale voice contract", they almost always mean a SIP-delivered service.

The reason the older term survives: contracts, settlement, fraud control, and route quality are concepts that pre-date IP voice. The plumbing changed; the commercial structure largely did not.

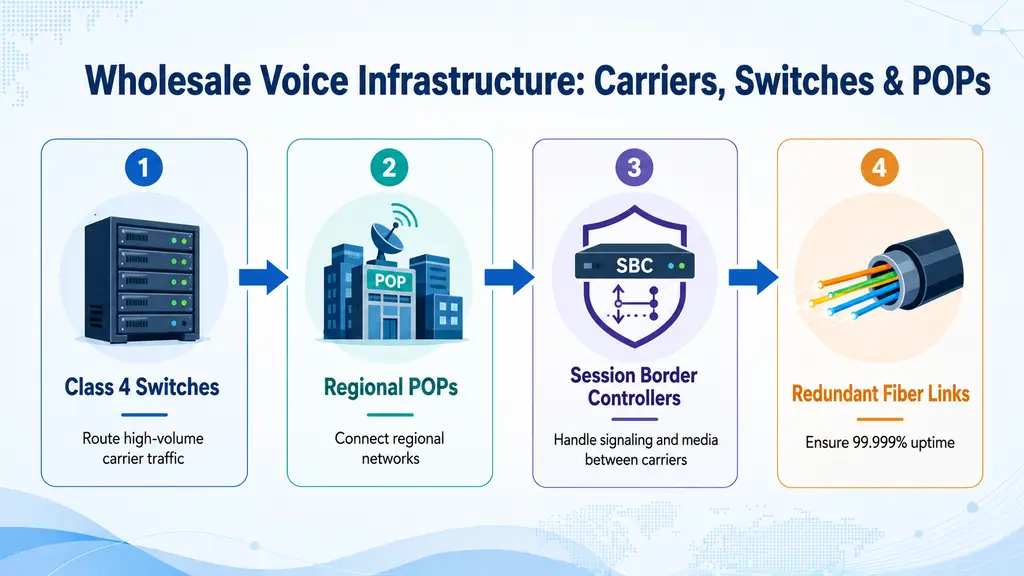

Carriers are categorised by where they sit in the wholesale supply chain.

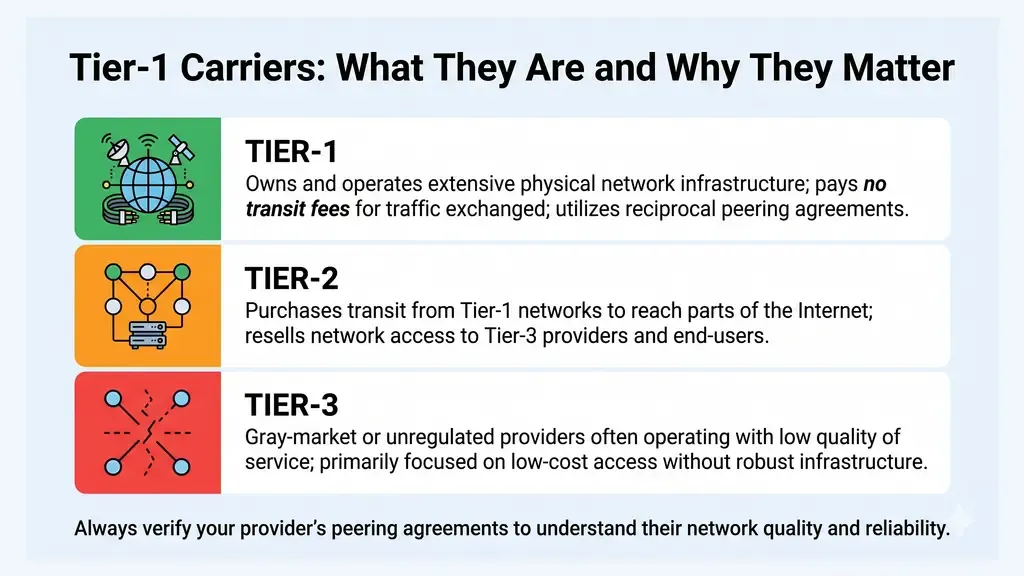

Tier-1 carriers have direct settlement agreements with the destination operator — no intermediaries. Verizon to Deutsche Telekom for traffic to Germany is a Tier-1 route. The premium for Tier-1 is real: the highest answer rates, the lowest post-dial delay, the most reliable CLI preservation, and the cleanest billing.

Tier-2 carriers buy capacity from Tier-1s and resell it downstream. The quality is still solid but slightly degraded — an extra hop adds latency, and the CLI sometimes gets reformatted. Margins are thinner, so reliable Tier-2 routes still cost meaningful money.

Grey routes are unauthorised termination paths that exploit settlement gaps. A SIM-box farm in a third country accepts calls from a wholesale buyer, then re-originates them on local mobile networks, dodging international settlement entirely. Grey routes are cheap and often illegal in the destination country. They are also unreliable — operators detect and blackhole them constantly.

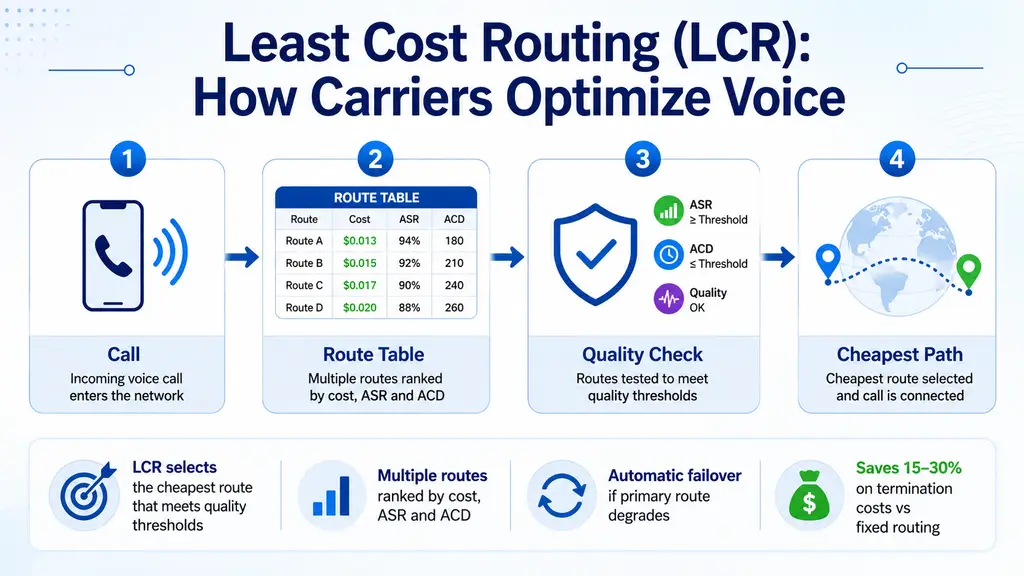

LCR is the engine that picks which interconnect to use for each call. A wholesale platform might be loaded with rate cards from a dozen upstream carriers. For each new call, the LCR engine looks at the destination prefix, the rates available, the quality scores on each route, and the call's own priority — then picks the cheapest route that still meets the SLA.

The math is more interesting than it sounds. The cheapest rate is rarely the best route. A carrier that quotes €0.0028/min to Germany on a grey route might have a 28% ASR; the Tier-1 route at €0.0085/min has a 62% ASR. Per completed call, the "expensive" route is cheaper. Mature LCR engines optimise on landed cost per answered call, not on per-minute price.

LCR also rotates traffic continuously. If route A starts degrading at 11 AM — its ASR drops from 60% to 40% — traffic shifts to route B within minutes. A good wholesale platform makes routing decisions on every single call, not in batched updates.

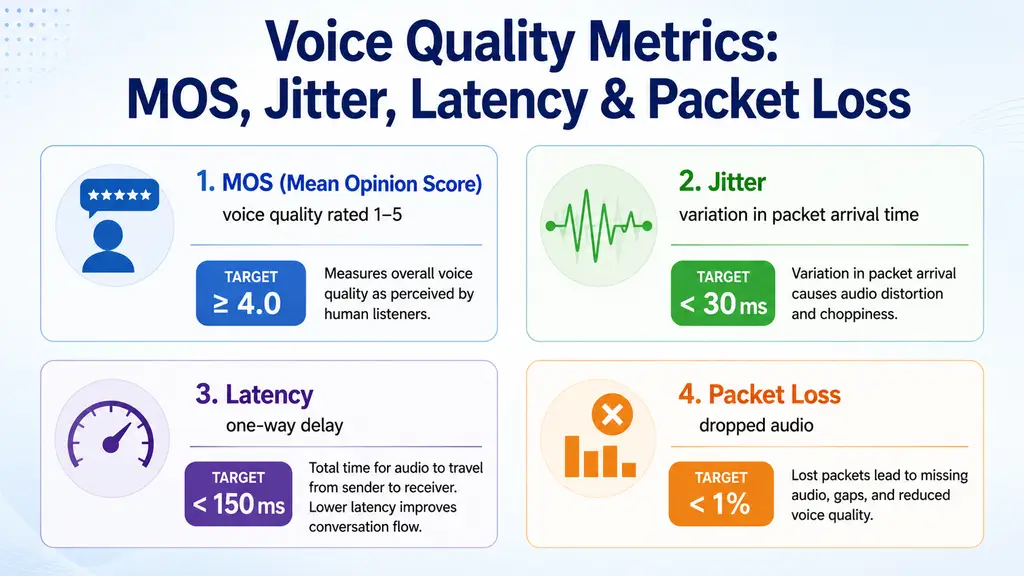

The single number everyone wants is MOS: Mean Opinion Score. It runs from 1 (unintelligible) to 5 (perfect). For business voice, 4.0 is excellent, 3.6–4.0 is acceptable, and below 3.3 is noticeably degraded.

MOS is derived from four underlying metrics:

Any serious wholesale buyer monitors MOS continuously on a sampled basis. A route that scored 4.2 in week one can degrade to 3.4 in week three without any commercial announcement — that's the signal to renegotiate or re-route.

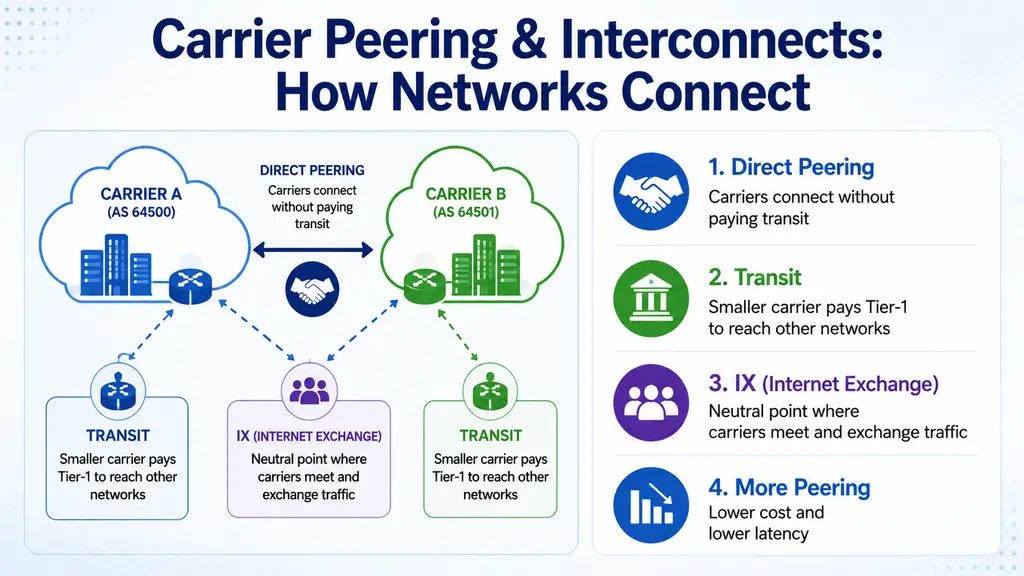

Voice peering is direct SIP interconnect between two carriers at a neutral exchange — an IX — where each agrees to terminate the other's traffic at a pre-negotiated rate. It is the voice equivalent of internet peering at an IXP.

Peering at an IX cuts out the transit carrier in the middle. Two regional operators that both peer at LINX in London can exchange traffic with one hop instead of three. The result: lower per-minute cost (because no transit margin), better call quality (because fewer hops), and faster fault recovery (because the interconnect is one cable in a colocation cage, not a multi-carrier path).

Major voice IXs include the Voice Peering Fabric, BroadCloud, and a long list of regional exchanges. Peering at an IX is a fixed-cost commitment — port fees, cross-connects, IX membership — so it makes sense once your traffic to a given peer exceeds the break-even against transit pricing. For most wholesale buyers, that threshold is reached only on a handful of corridor routes.

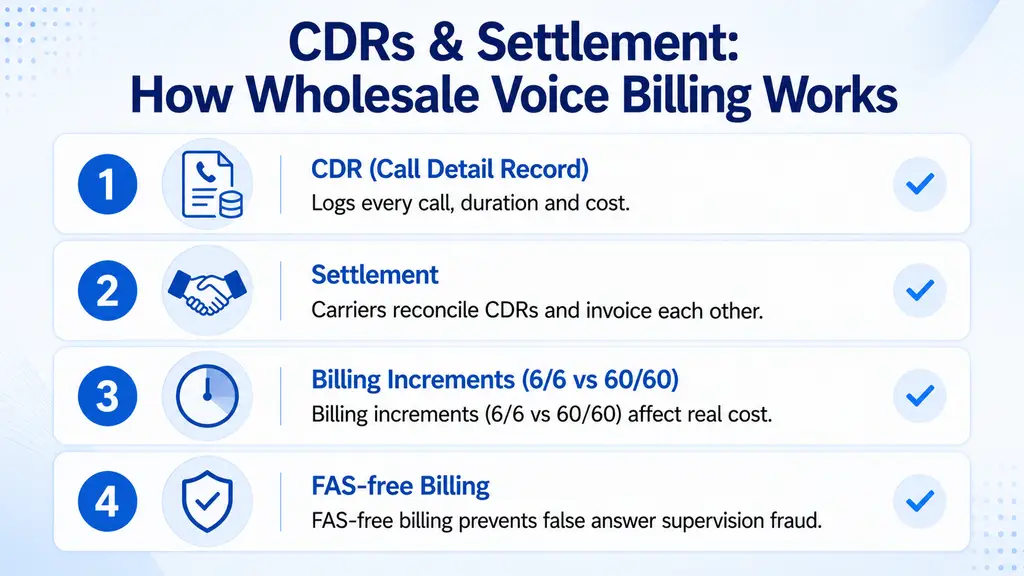

Settlement is the monthly reconciliation of traffic between two carriers. Each side submits its CDRs (Call Detail Records) of traffic terminated to the other, the per-minute rates are applied per destination, the totals are netted, and one party pays the other the difference.

Settlement disputes are routine. Carrier A claims it terminated 4.2 million minutes; carrier B's CDRs show 3.9 million. The 300,000-minute gap is usually a mix of dropped CDRs on one side, calls that completed but did not signal back properly, and a small slice of pure fraud (calls that were billed but never connected). Settlement audit clauses in wholesale contracts spell out how disputes are resolved — usually by handing both CDR sets to a neutral mediator and matching them call-by-call.

The reason CDR audit access matters: without it, you have no way to verify the bill you are being asked to pay. Always negotiate self-serve CDR audit tools into the contract. A reputable wholesale provider offers them as standard.

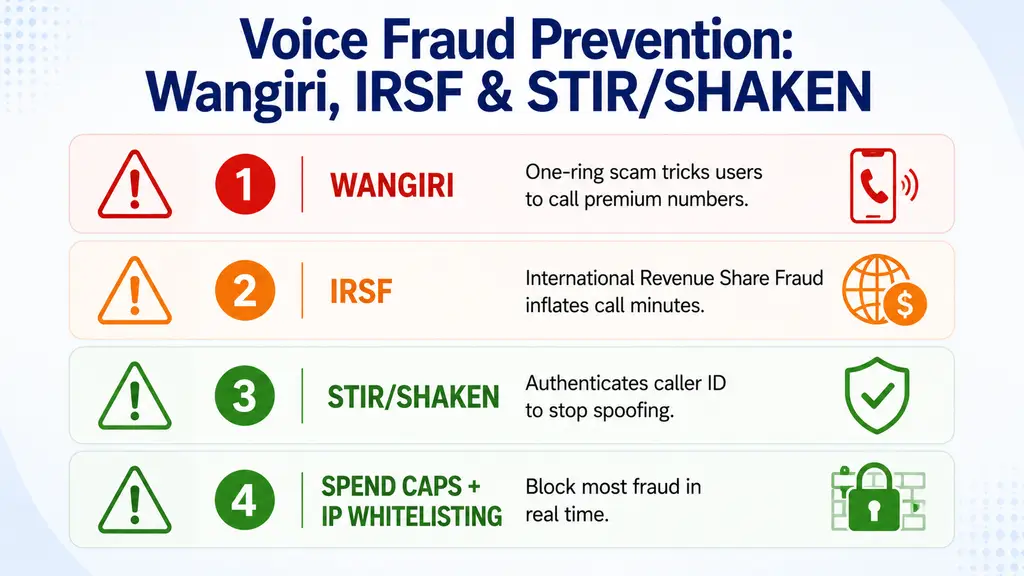

Wholesale voice attracts a specific family of fraud patterns. The three biggest:

Wangiri ("one-ring" in Japanese) — fraudsters originate one-ring calls to thousands of consumers from a premium-rate number. Some fraction call back, the call connects to a premium destination, and the originating carrier collects the inflated settlement. The victim sees a $20 charge on their next bill.

IRSF (International Revenue Share Fraud) — a compromised PBX is used to place thousands of expensive calls to premium destinations the attacker controls. The victim's carrier owes settlement to the destination; the attacker collects a kickback from the destination operator. Single incidents have cost enterprises over $1M in a single weekend.

Toll fraud — compromised SIP credentials, weak passwords, or open PBX ports used to place high-cost international calls. The pattern is well-known and 100% preventable with per-destination spend caps, IP whitelisting, and anomaly detection. A wholesale carrier that does not offer these as default controls is not a serious operator.

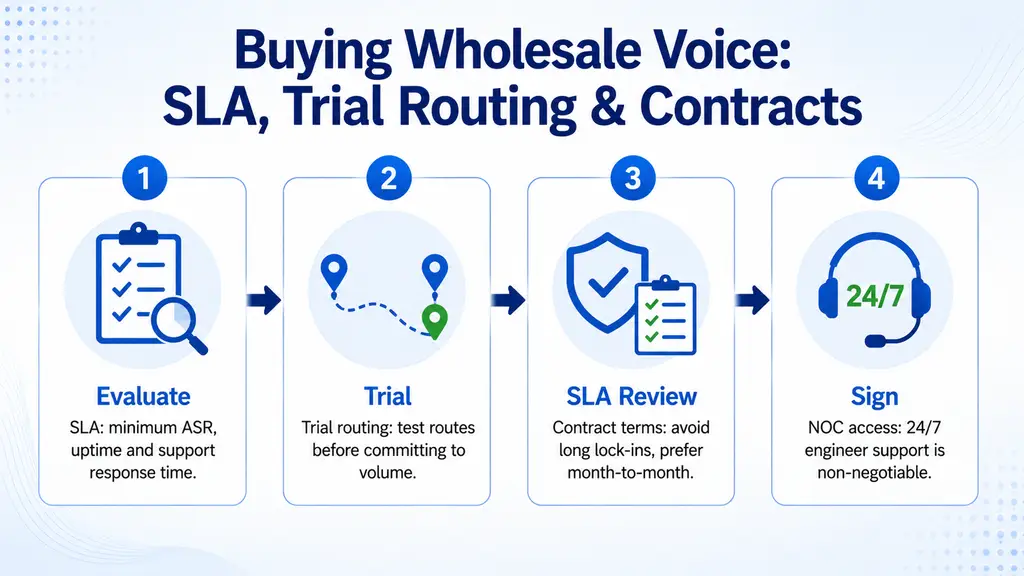

Five things separate a good wholesale voice contract from a painful one.

1. Insist on transparent rate cards. A rate card with thousands of destination prefixes, updated weekly, with timestamped change history. If you have to email for rates, you do not have a real wholesale relationship.

2. Demand CDR audit access. Self-serve, no support ticket required. Every call, every leg, every rate applied.

3. Test before you commit. Run 10% of your traffic through a new provider for two weeks before you migrate any further. Measure ASR, ACD, PDD, and MOS against your incumbent. The pre-sales numbers will be the marketing number; you want the live one.

4. Read the dispute and chargeback clauses. What is the SLA on resolving a billing dispute? What is the maximum chargeback period? These clauses look boring until you need them.

5. Meet the NOC. Wholesale voice has no support hours. A 24/7 NOC, with a real person on the phone in under 90 seconds at 3am, is the minimum bar. Test their response time during sales — not after you sign.

Wholesale voice is a commodity market — voice minutes priced by destination, billed by the second, settled monthly. But like any commodity market, the quality of what you buy varies wildly from one supplier to the next, and the difference shows up in your customers' answer rates long before it shows up on the invoice. The operators who win are the ones who measure what they bought as carefully as they negotiated what they would buy.

If you remember three things from this guide, make it these: insist on real Tier-1 routes for any traffic where call quality is a customer-facing metric, monitor ASR, ACD, PDD, and MOS on every route continuously rather than at procurement time, and treat fraud controls as table-stakes. A wholesale voice provider that meets that bar will be a quiet line in your budget for years. One that does not will eventually announce itself in the form of a 3am NOC call you cannot get answered.

Wholesale voice is the broader business of selling voice minutes between carriers — it includes legacy TDM voice as well as IP voice. Wholesale VoIP is the IP-only subset, where calls travel over SIP and IP transport. Today the vast majority of wholesale voice traffic is also wholesale VoIP, but the two terms are not perfect synonyms in carrier procurement contracts.

A Tier-1 carrier has direct settlement agreements with the destination operator in a given country, with no intermediate carriers in the route. Tier-1 routes have the highest answer rates, lowest PDD, and the most reliable CLI preservation — but the highest per-minute cost.

MOS is a 1-to-5 score that quantifies perceived voice quality on a call. 4.0+ is excellent, 3.5–4.0 is good business quality, below 3.0 is noticeable degradation. MOS is computed from packet loss, jitter, latency, and codec — carriers and wholesale buyers use it as the single-number quality benchmark.

LCR is the routing engine that picks the cheapest available route for each call destination in real time. A wholesale carrier loaded with rate cards from a dozen interconnects uses LCR to send each call down the lowest-cost route that still meets the buyer’s quality SLA — automatically re-routing as rates change.

Carriers settle traffic monthly. Each carrier submits CDRs (Call Detail Records) of traffic terminated to the other, the per-minute rates are applied per destination, and the difference is net-settled. Disputes are resolved against the underlying CDRs — which is why CDR audit access is a standard wholesale contract clause.

Voice peering is a direct SIP interconnect between two carriers, usually at a neutral exchange point (an IX), where each agrees to terminate traffic for the other at a pre-negotiated rate. It cuts out intermediate transit carriers, lowers per-minute cost, and improves call quality.

Tier-1 A-Z termination across 200+ countries, transparent weekly rate cards, MOS-monitored routes, self-serve CDR audit, and a 24/7 NOC that picks up in under 90 seconds.